Many individuals recognize the need and importance of planning for the future, but what if the plan you and your family have been working toward comes to an abrupt halt? Life insurance can play an important role in a financial plan and therefore, the amount of coverage should be based on the goal it is intended to fulfill. A group life insurance policy through work is a valuable employee benefit, but if you have a real need for coverage, the amount provided is usually not enough.

So, how much is “enough”? It should be enough to provide for your loved ones in the event of your passing in coordination with your individualized goals. You may have heard of the “10 Times Rule,” which is a general rule of thumb that life insurance coverage should be roughly the equivalent of 10 times your annual income. We would suggest that while this may be a good start, a life insurance calculation should be based on a more in-depth calculation of your individual goals and objectives.

The life insurance calculation begins with determining what goal you need the insurance to cover. For many individuals, this includes things like paying off debt, satisfying a mortgage, covering monthly expenses and addressing future objectives like retirement and college educations. Before we can begin the life insurance calculation, we must address certain questions such as: If one spouse passes away, will the surviving spouse continue to work full time? Would there be additional expenses like childcare to cover? Will the insurance need to cover retirement savings for the surviving spouse? What about college? Is there a gap between your monthly expenses and your surviving spouses’ income?

Once the goals have been clearly defined, we can calculate the amount needed to fully cover the current and future goals. The time value of money calculation that is used factors in the expected rate of inflation and return on investment, while also factoring in the timing of expected distributions. This calculation allows us to project, as accurately as possible, what an individual will need to ensure all of their objectives would be met at death.

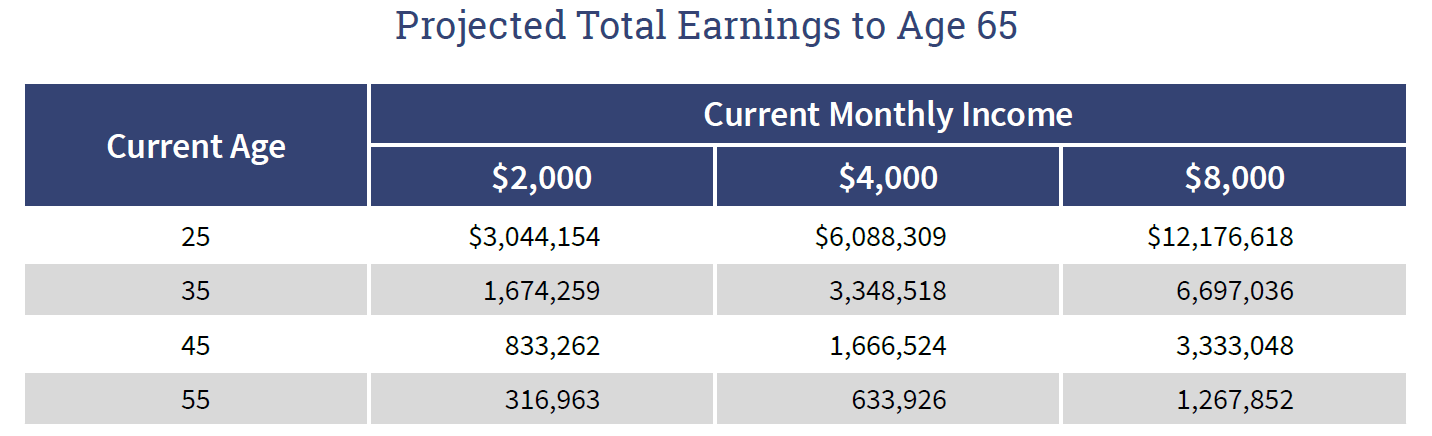

You might think that $500,000 or even $750,000 in term coverage is sufficient, but you may be surprised to find that this is not enough to cover the amount determined by your personal needs analysis. Take the chart below, for instance. A 45-year-old with a monthly income of $4,000 is projected to earn $1,666,524 during their career assuming retirement at age 65 and a 5% annual wage increase.

While a $500,000 policy would be a good start, you can see how it may fall well short of paying off debt obligations, supplementing the income of the surviving spouse, and covering other objectives such as college funding and retirement savings.

Affordability of the policy may also play a role in your decision process. The good news is that life insurance needs can usually be covered in a very cost-effective manner through term insurance. A relatively young and healthy individual typically can lock in their insurability and take advantage of more affordable rates for large coverage amounts. While insurance becomes more expensive for older individuals, the price is often worth paying if the insurance needs are there.

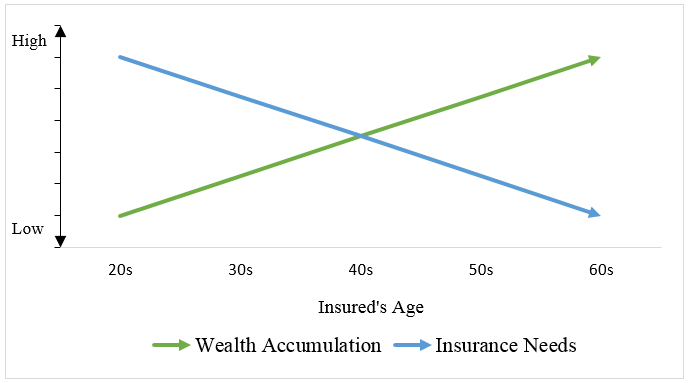

As life progresses, your financial needs will evolve accordingly. A young individual with a family, at the early stages of wealth accumulation, will typically have higher insurance needs, based on survivor needs and their expressed goals. As time progresses and wealth accumulation occurs, the need for insurance is typically lower as the investment assets will provide for the needs of the family.

Once life insurance is in place it should be reviewed periodically. It is important to recalculate your personal desired death benefit after major life events such as marriage, birth of a child, divorce, death in the family, taking on additional debt, wealth accumulation, changing jobs, or retirement. These events will impact the amount of coverage needed for a successful long-term financial plan.

Life insurance plays an integral role in the financial plan for many individuals, families and businesses. We understand that deciding the amount of coverage, combined with identifying the appropriate type of insurance (term or permanent), can be difficult to navigate. Because we do not sell insurance, our team of CFP® Professionals here at Voisard Asset Management Group can be an objective resource to help assess your individual needs. If you find that there is a gap between your coverage and your goals, we would be happy to provide you with a trusted insurance professional to assist in implementing the coverage you need.