Retirement fund fees are complex. Between administration, investment management, record-keeping, consulting, revenue sharing, sub-TA and 12b-1, it isn’t always clear to plan participants or plan sponsors exactly the purpose and value of all of these fees. It also isn’t clear as to who these fees are benefiting and who, therefore, should pay for them.

ERISA Section 408(b)(2) states that plan fiduciaries must determine whether the service agreements and compensation of service providers are “reasonable.” The rule requires service providers to supply plans with disclosures to help them determine if fees are “reasonable.” Voisard Asset Management Group helps fiduciaries with this complex determination by identifying:

- Total plan cost and its component parts

- The primary drivers of retirement plan pricing

- The role and appropriateness of revenue sharing

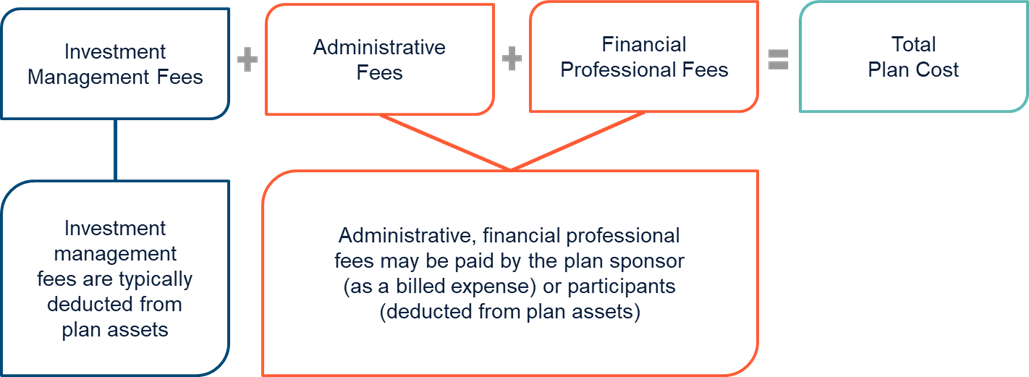

Cost Components

The three main components are administrative fees, investment fees and financial professional fees. Financial professional fees are often paid by the plan sponsor. Administrative fees can be shared between the plan sponsor and the participants. Investment fees are typically paid by participants and deducted from plan assets.

Primary Pricing Drivers

Several key factors can impact plan pricing. Typically, the larger the plan in terms of assets and average participant account balance, the lower the plan fees. Other factors include:

- Number of plan participants

- Service requirements

- Plan design features

Revenue Sharing

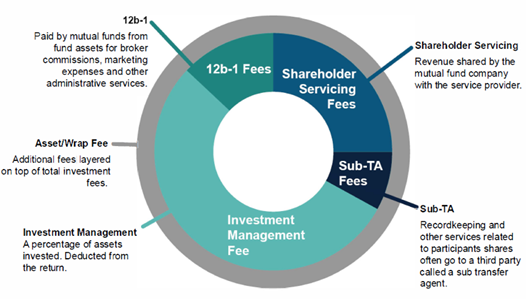

Revenue sharing includes payments made by investment managers to service providers or plan consultants for a portion of the revenue generated from the management of a particular fund or funds. Historically, such allowance may or may not be known to a plan sponsor. Regardless, it’s imperative that plan sponsors with fiduciary oversight of their organization’s retirement plan understand the distribution systems that most investment management organizations use and how they share revenue.

The most common forms of revenue sharing can include 12b-1 fees, shareholder servicing fees and sub-transfer agent (sub-TA) fees. In some instances, a portion of the investment management fee for proprietary funds may include some revenue sharing. The diagram below illustrates potential fund expenses.

Fiduciary Best Practices

Best practices dictate that plan fiduciaries must go through a prudent, comprehensive, and measurable process of monitoring and documentation to ensure that only reasonable fees are being paid. This process includes:

- An experienced consultant with expertise on retirement fund fees & their components

- Analyzing and documenting all fees from service providers

- Reviewing fees annually compared to normative data as a second opinion on reasonableness

- In-depth, live-bid benchmarking of fees, services and investments compared to alternative providers every three years to ensure reasonableness, competitiveness and appropriateness of fees and services

If you would like to have a free benchmarking report of your current plan fees, or if you would like to learn more about our practice, please reach out to John Hays either by phone at (616) 988-5778 or e-mail at jhays@voisardgroup.com.